The weeks between writing each monthly President’s Column always seem to pass quickly. What appears to move even faster, however, are events unfolding on the world stage. Fewer than 30 days ago, discussions around the energy transition, the 2 to 4 million barrels of crude “on the water,” and a short-term decline in demand were common themes in many conversations.

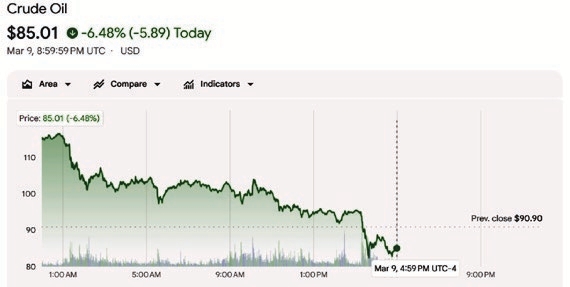

In the past two weeks, the oil supply calculus has shifted dramatically. The volatility in oil prices should remind us that, in many respects, emotion still plays a significant role in price formation. A $40 swing in oil prices in a 12-hour period on March 9 is compelling evidence. By comparison, Henry Hub natural gas prices declined $0.40/million British thermal units (MMBtu) over the same period. On a percentage basis, that represents a more than 30-percent move for oil and a negative-10-percent move for gas (figure 1). Today oil is trading near $96 a barrel (up 11 percent), and global sentiment has shifted toward concerns over supply scarcity following the closure of transit through the Straits of Hormuz.

The impact on the gas market is being felt primarily in Europe as liquefied natural gas export from the Persian Gulf has stopped and Dutch TTF prices are $17 MMBtu. A stark difference from Henry Hub which is in the $3 range.

Just as the time between monthly columns seems to accelerate, global circumstances can change at an even higher frequency. Over the past year, markets appeared to discount political risk in favor of the belief that oil was oversupplied. Those who raised concerns about risk were rarely the ones trading physical supply. For more than a decade, the world has benefited from increased production and relatively slow demand growth. Yet, even slow growth is still growth, and eventually many small increments accumulate into something much larger. As we saw in 2020, supply chains can become vulnerable quickly. This is why the energy discussion has become about security for every economy.

How long this ”shortage” can persist remains an open question. It currently is not a production shortage, but more of a distribution dilemma. As the uncertainty continues, production will be shut in and the system will begin to back up. I doubt that most people truly understand that production, refining and distribution of oil and gas is its own ecosystem. There are multiple counter dependencies and links in a distribution chain. A single link can have a large impact over a long enough period.

The future impact on the global economy depends on developments over the next few months, given that roughly 20 percent of the world’s oil and LNG supply passes through a 30-mile-wide stretch of water.

There is one certainty: price volatility is likely to continue until commerce ultimately prevails over chaos.

Consistency Always Triumphs

My training as a geoscientist has shaped how I view risk and uncertainty. The more I learn, the more aware I become of the gaps in my own understanding – whether macroeconomic, political, commercial, or technical. I read articles and posts, listen to podcasts highlighting the latest innovations or ideas poised to “revolutionize” the energy supply chain. What I rarely read or hear about is what is working right now. That rarely qualifies as newsworthy. Reality is often perceived as commonplace, mundane. But isn’t that where most of life happens?

Between the extremes of great success and notable failure lies the steady rhythm of daily work. We only become aware of it when it stops. I am sure we can all remember the last time the power went out – something most people in the United States take for granted.

During graduate school, I had the privilege of working for Amoco while pursuing my degree. I often felt overwhelmed, convinced I was never going finish my thesis and graduate. At the same time, I was struck by the geologists on my team who worked quietly and consistently, adhering to an unremarkable 8-to-5 schedule. Weeks or months would pass and they would produce maps of remarkable quality and insight. I realized there was no singular moment of insight driving that outcome. It was simply steady progress day after day. Consistent application of skill and observation led to clarity – both in what map to make and why it mattered.

Today, two narratives are gaining traction around oil prices. One suggests that prices will fall once geopolitical conflicts stabilize, as we briefly saw following an errant press release last week. The other points toward a longer-term supply shortage. While this may unfold over a longer cycle, many analysts are focusing their concern about a potential 20-million-barrels-of-oil-per-day production shortfall over the next 10 to 15 years. “Peak shale” is often a rationale for the decline, but the data certainly do not indicate this is the case. It is price that will continue to drive Lower 48 activity and the continued improvement in operating efficiency. We might see a plateau in production, but I would not underestimate the innovation of the oil and gas industry given the United States is close to 14-million-barrels-per-day production.

Both narratives can be true – just not at the same time. As with discussions around climate, the time frame under consideration is critical. Looking toward 2040, the industry is expected to experience a cumulative production decline of approximately 20 million barrels per day.

That is the nature of oil and gas production. What is not expected (by most), however, is a corresponding decline in demand.

That reality raises a fundamental question: Where will that supply come from, and who will discover it?

Focus on Today

I’m reminded of Mike Tyson’s observation: “Everybody’s got a plan until they get punched in the face.” It neatly captures the uncertainty inherent in our business. Market disruptions and political turmoil are nothing new and we think we have a plan to mitigate uncertainty and reduce risk. However, the current challenges of conflict have exposed longstanding bottlenecks and vulnerabilities in the global supply chain. We’ve known about these challenges for years. The difference now is that the cost of inaction is becoming increasingly clear.

AAPG is embarking on several new initiatives to address the future of geoscience: The AAPG Academy, further collaboration with the Society of Exploration Geophysicists and the Society of Petroleum Engineers, improving the Imperial Barrel Award competition, expanding the Presidents Tour outreach to universities to the Alumni Tour supporting AAPG members’ re-engagement with their alma mater to share their industry and career experience to the next generation of geoscientists, and adding new modules to the Imperial Barrel Award competition more aligned with current industry practices, and providing a broader publication platform to give members greater access to a wider range of publications and AI-enhanced large language models to streamline research and access to education.

So, let’s focus on what we can change today. If Nassim Talib is right, we will not see a glut any time soon.