In the February 2026 Explorer, I wrote about recent staff changes and the finances associated with these decisions. Since that article, I have had several members approach me and suggest that AAPG is in financial distress. This is not the case and is a misread of my article. In my article, I pointed to historical uneven net income performance and asserted that changes are needed for AAPG to be more financially balanced. I also discussed that our emergency cash reserves have been well managed and enjoyed a positive market environment, which have helped minimize our underperformance. Furthermore, I argued that greater fiscal discipline must be applied. Lastly, I suggested that members are looking to experience membership at a local level, and this required us to pivot our staff resources from being more administrative to being more member-services centric. The staffing changes also helped us lower our administrative costs.

Please let me explain more about how our investments have improved our position, but not made us bulletproof.

Nonprofit Budgeting

Each year, AAPG sets a budget. Our fiscal year runs from July 1 to June 30. The typical goal of a nonprofit professional association’s budget is to balance revenues and expenses while maximizing member benefits. When revenues exceed expenses, cash reserves are built or the excess is spent on additional member benefits. New staff might even be added. When expenses exceed revenues, either cash reserves are drawn down or member benefits are reduced. On occasion, staff cuts might also have to be made. Staffing changes should be the last resort to ensure operational continuity.

Cash Reserve Usage

AAPG is blessed to have sizeable cash reserves. Currently, our investments total about $12.6 million and are managed by a fiduciary under the oversight of an Investment Committee. If expenses outpace revenues, AAPG executive leadership requests a withdrawal from these investments to cover costs. This occurs off the income statement but is recorded on the balance sheet. These cash movements are largely about cash-flow management and paying our bills.

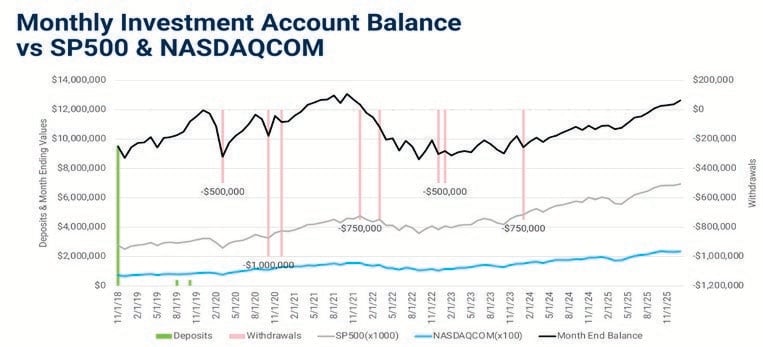

and the NASDAQ Composite by a factor of 100 to make them more legible on the graph.

Regretfully, investment withdrawals have been a common occurrence since March of 2020, when the COVID pandemic hit. Figure 1 below highlights investment withdrawals versus annual net income (revenue minus expenses).

What has been impressive is the ability of the Investment Committee to offset these episodic, unplanned withdrawals. Since 2020, eight withdrawals totaling $5.75 million have been made to cover budget shortfalls. In November 2018, the ending monthly balance in our investments was $9.58 million. At the end of January 2026, our investment balance was $12.64 million. Figure 2 below charts our month-ending balances over time against the SP 500 and the NASDAQ Composite indices.

Also noted on the figure are the investment withdrawals. By and large, our investments have matched or outperformed market indices.

Cost of Investment Withdrawals

Does this type of investment performance mean we can continue business as usual? The answer is “no.” Although the emergency cash reserves are there to backstop the finances of AAPG, they are not a cure for poor fiscal or operational management. Obviously, had we not withdrawn the money, we would have a larger investment fund. Some estimates value our investments at approximately $36 million today had we not extracted capital to cover deficits. Going forward, we are exploring the possibility, if needed, of taking a small scheduled percentage withdrawal of 4 percent annually. This is a common practice for many non-profit associations that are fortunate enough to have a sizable investment portfolio.

Investments Serving Their Purpose

Committee chairs and Executive Committee members have counseled me not to focus on what could have been had we not taken the investment withdrawals. The cash reserves have performed as intended. They have enabled AAPG to sustain itself and to backstop financial shortfalls. Prior Executive Committee members have gone further and encouraged me to budget with investment withdrawals in mind. Candidly, I struggle with this approach of utilizing our cash reserves to pay routine operational costs and see a detrimental investment opportunity costs for operating in this manner.

Conclusion

As we head into budget season, please know that with the recent Bylaw changes, the executive director is responsible for the Association’s spending and financial health. I take this very seriously and will be working hard to maintain a balanced budget that delivers tangible member value at the local level. Additionally, I will be working with the Investment Committee to either create a planned investment withdrawal schedule or I will be working to prevent the need to withdraw emergency cash investments.

One Last Point

Please note that the cash reserves discussed above are not related to the AAPG Foundation. The Foundation is an entirely separate organization with a different nonprofit tax model. They have an endowment greater than $70 million and are dedicated to giving to geoscience educational causes. The AAPG can only receive funds from the Foundation if its request for educational program support is granted by AAPG Foundation. The Foundation also has an ongoing capital campaign to increase their endowment. This campaign will not impact AAPG’s invested cash reserves but is for the worthy cause for earth science education.