Two factors have led some companies to downplay the importance of exploration during the past 20 years. First, the shale revolution starting in 2008 gave some companies, especially American producers, a unique growth vehicle. Second, initiatives on climate change and the energy transition caused strategic change with low-carbon energy, especially in Europe.

Now, executives at leading European international oil companies, including BP and Shell, have realized that they might have gone too far and too fast in the energy transition. There are also signs that shale production in the United States might be peaking, especially when oil prices are low. Exploration has been given renewed importance, but it is not without some challenges.

I recently hosted an AAPG Academy webinar entitled “Future of Exploration,” featuring expert speakers Aatisha Mahajan, lead analyst for exploration at Rystad Energy, and Bryan Ritchie, vice president of exploration for BP. They shared key insights around the current opportunities and challenges in exploration. Here are some of the highlights of that dialogue and related exploration trends.

2025 Was a Challenging Year, But Acreage Reload Provides Promise for the Future

Mahajan stated that 2025 appears to be the least successful exploration year since 2019, in terms of conventional oil and gas volume discovered.

Estimated total volume discovered in 2025 amounts to 5.4 billion barrels of oil equivalent, the fourth consecutive yearly decline since 2022 and nearly three times less than the total volume discovered in 2019.

The accuracy for exploration success sometimes needs time to be verified, as some operators have not yet released official volume estimates. For others, appraisal drilling campaigns are yet to be completed. Nonetheless, Rystad’s data showed a negative trend over several years.

Rystad also showed that the commercial success rate for 2025 was 26 percent, down from 41 percent in 2023, and 27 percent in 2024.

India and Algeria were by far the two leading countries awarding new exploration acreages in 2025, both with more than 100,000 square kilometers. Total conventional acreage awarded in 2025 was 826,000 square kilometers, the highest since 2020, reflecting many companies’ refocus to exploration, despite a relatively low average oil price of $69 per barrel in 2025.

Corresponding to the active licensing activities in India and Algeria, ONGC, Sonatrach, and Oil India led the way, capturing the largest amount of acreage. Among the international oil companies, ENI and Chevron captured the most new exploration acreage, each with more than 20,000 square kilometers.

Increased exploration expenditures, especially in acreage capture and seismic acquisition, processing, and interpretation will take time to turn into actual volume discovered. Leaders expect AI and machine learning will shorten the cycle time from acreage capture to volume discovery, from four to six years to two to three years.

IOCs Step Up Exploration Efforts

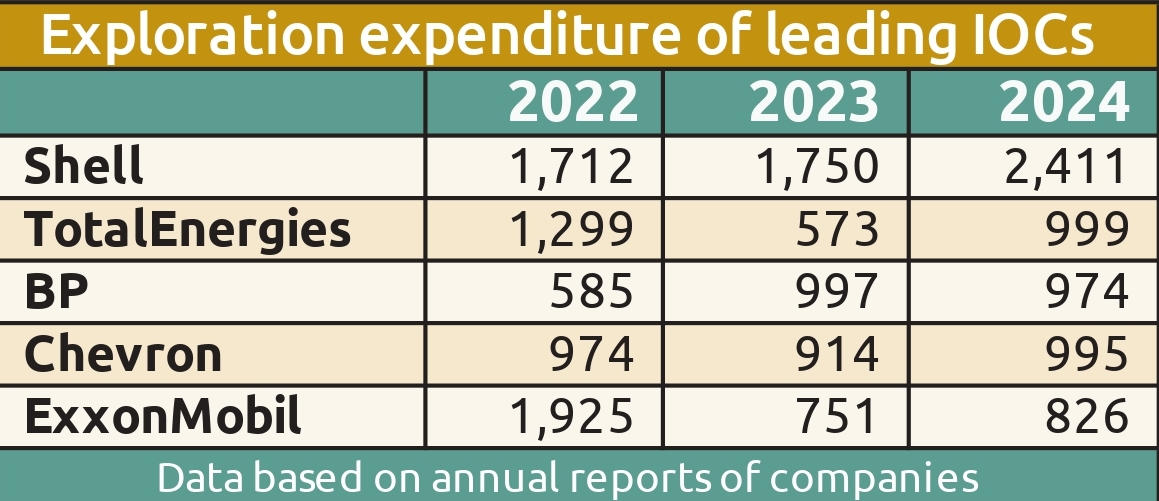

Since 2023, BP has increased exploration spending, doubling from around $500 million for annual exploration in 2021 and 2022, to roughly $1 billion per year since 2023. Its Bumerangue oil discovery in Brazil’s Santos Basin in 2025 has found an estimated 8 billion barrels of liquids in place, the largest discovery for BP during the past quarter century. Ritchie said that BP will start its appraisal campaign for the Bumerangue discovery during the second half of 2026. BP holds 100-percent equity for this significant future value generator.

Shell has been the highest investor in exploration among the majors, with more than $2 billion in annual exploration budget in 2024, as revealed from its annual reports. The biggest European major hopes to have its own breakthrough discoveries soon.

French major TotalEnergies has an annual expenditure budget of roughly $1 billion. In December 2025, TotalEnergies was the winner in Galp’s auction for its Mopane oil discovery in Namibia. TotalEnergies also plans to take final investment decision for its Venus oil discovery in the Orange Basin and is on its way to becoming the dominant IOC in this emerging African oil-producing country.

Chevron has also upped its exploration efforts significantly. In 2024, Chevron said that its reserve replacement ratio was -4 percent, while the proven reserve-to- production ratio declined from 10.2 years in 2022 to an alarming 8.1 years in 2024.

The second-largest American company appears determined to continue growing through exploration. In November 2025, it hired Kevin McLachlan, formerly from Murphy Oil and TotalEnergies, to be its vice president of exploration.

During its market update call from the same month, Chevron said that “Over the next few years, we plan to increase annual spending by approximately 50 percent, with a focus on the Gulf of Mexico (America), South America, West Africa, and the Mediterranean.”

Chevron also captured new acreage in Brazil, Uruguay, Namibia, Greece, and Libya. Alongside BP, Chevron was one of the top winners during the latest Gulf of Mexico (America) lease sale in December 2025.

ExxonMobil has been the most consistent with its exploration expenditure, averaging about $ 1 billion per year since 2022. ExxonMobil has also had a significant advantage over its peers with more than 11 billion barrels of oil reserves discovered in Guyana since 2015. Its proven reserve stands at 19.9 billion as of year’s end 2024, with a healthy reserve life of 12.7 years.

Many trailblazing independent explorers, such as Anadarko and Kosmos Energy from the United States, as well as Tullow Oil from the United Kingdom, have lost some of their luster recently, partly because of the success of U.S. shale. Anadarko was acquired by Occidental in 2019.

When asked “who are the ‘Anadarkos’ of today,” Ritchie and Mahajan pointed to Murphy from the United States and Rhino Energy Resources from South Africa. Murphy made a significant oil discovery in offshore Vietnam last year, and Rhino Resources made a key oil discovery in Namibia.

The South Atlantic Will See Much Action in 2026

This year is set to be one of the most exciting years for global exploration. And the industry is anxious to see a significant turnaround toward higher success rates and bigger volumes discovered.

According to Rystad, exploration expenditure is estimated to be $55 billion in 2026, and drilling expenditure in frontier basins will top $10 billion – both are at their highest levels since 2019. Infrastructure-led exploration and near-field exploration will be between $7 and 8 billion with the balance in appraisal and other exploratory drilling. Close to $30 billion will be spent in West Africa, South America, Asia, and North America.

Key countries and basins to watch include Brazil, especially its Equatorial Margin, Uruguay in South America, Libya, Namibia, South Africa, Angola, and Somalia in Africa, Turkey, Bulgaria, Greece, and Greenland in Europe, Indonia, Malaysia and India in Asia, and the Gulf of Mexico (America) in North America.