No, we do not seem to be exploring enough to continue to guarantee energy security while population, economies and energy demand continue to grow. This risk is due both to externally-imposed restrictions and to self-inflicted wounds. Oil companies, financial institutions and governments have roles in dispelling energy security risks via stepped-up hydrocarbon exploration.

Oil and gas will be with us for the conceivable future. Renewable energy technologies other than hydroelectricity are evolving spectacularly fast and becoming cost competitive, but they have taken off from an extremely low basis. They indeed reached record output in 2024, but so did oil, gas, and even coal. Those renewables currently contribute just around 8 percent of the global primary energy matrix, while fossil fuels still supply more than 81 percent. Regarding electricity generation, they supply less than 16 percent, while fossil fuels still yield 60 percent.

This is because global energy demand continues its relentless growth, despite continuous energy efficiency improvements. For example, the artificial intelligence revolution that might help us reengineer our energy systems requires huge data centers with an insatiable hunger for energy and cooling water.

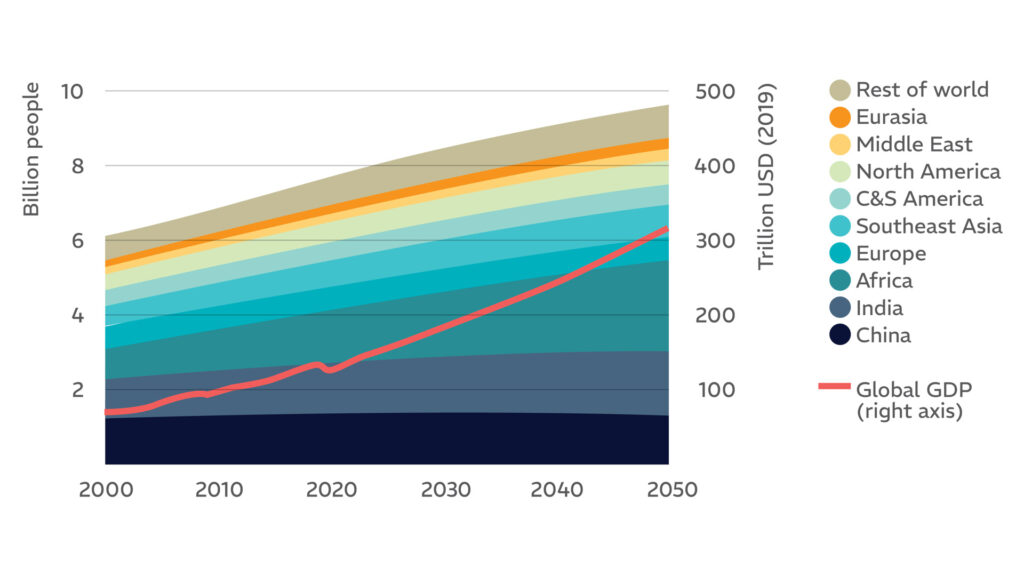

Global economic growth (measured as global GDP) is itself the compound of GDP/capita growth with demographic growth. It broadly outpaces demographic growth (figure 1) and drives energy demand growth. Demographic growth has certainly decelerated. However, having reached an inflection point earlier this century does not mean that it will decline anytime soon. We are still adding one million net people every six days. Earth has about 8.2 billion tenants today, it should reach 9.7 billion by 2050 and 10.3-11.2 billion by the end of this century.

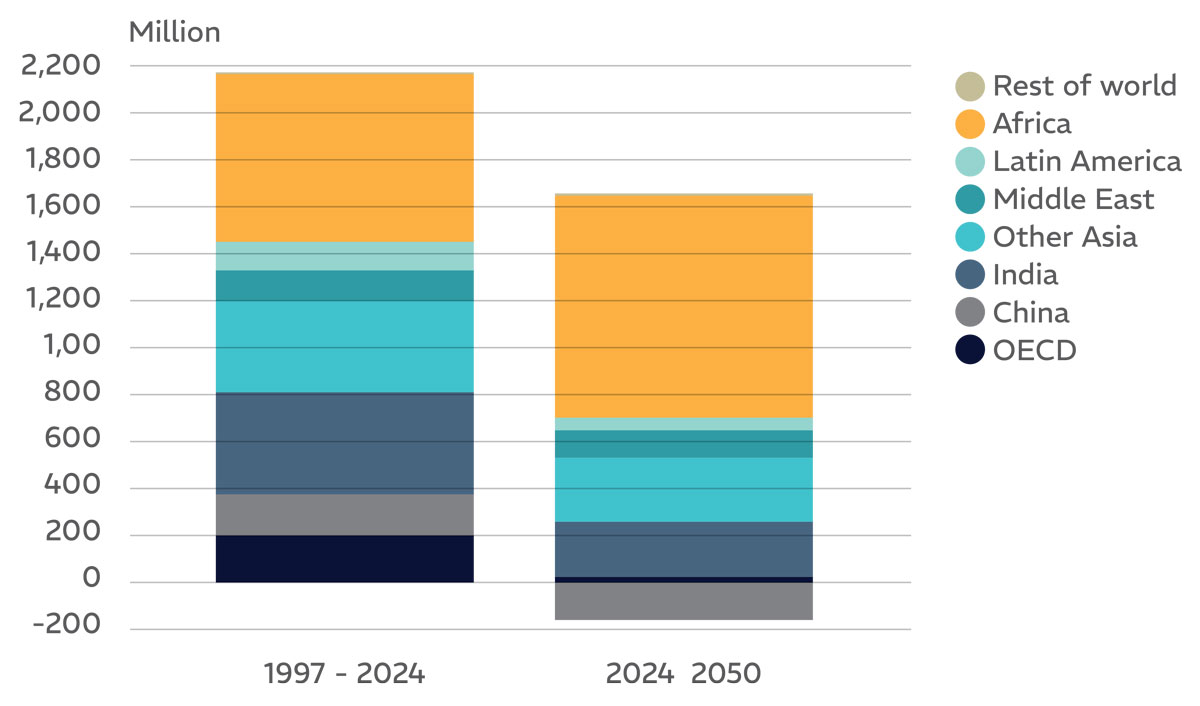

Granted that in the Organisation for Economic Co-operation and Development-group of countries and in the relatively most prosperous developing regions, fertility rates have fallen below their replacement rates; their past demographic pyramids now begin to look like columns. For example, the median age in the European Union has grown to 45 years and to almost 50 years in Japan. But in contrast, Africa’s relentless demographic growth continues (figure 2); its median age is now 19 years.

Countries in the “Global South” have not yet fully climbed the economic development curves to which they rightfully aspire. For example:

- Latin America and the Caribbean have 27 percent of their populations under the poverty line and 11 percent in extreme poverty. Still, 6 percent of their rural populations have no access to electricity and 8 percent still cook with wood, charcoal, or animal waste.

- The African region has 47 percent of its population in poverty and 28 percent in extreme poverty. Of its rural population, 56 percent have no electricity and 58 percent still also cook with biomass.

It is clear that, in varying degrees, countries must deal with urgent social priorities, including abating energy poverty. For reasons of scale, availability and cost, such socioeconomic development is bound to be more carbon intensive. The EU’s Carbon Border Adjustment Mechanism will thus unfairly penalize imports from the Global South.

Transition with Replacement? Or Evolution with Addition?

The term “dilemma” implies that there can be no universally desirable alternative per se, and that tradeoffs and pragmatic compromise are inevitable. As originally postulated, our energy “trilemma” looked like a metastable equilibrium system (not unlike trying to balance a soccer ball on one’s head). But lately, energy security and affordability are outweighing sustainability, further destabilizing the trilemma’s inherently challenging balancing act.

It is now evident that we are not experiencing a transformative transition; it is more about addition than replacement. In fact, the word “transition” also implies a radically different final state, while the ongoing process looks more like an evolution of our current state to one with significantly less emissions.

Fossil fuels and renewables are technologies with related supply chains that address diverse needs. Under the most realistic scenarios, renewable energies might support demand growth, but fossil resources shall continue to supply hard-to abate sectors with high energy intensities, long asset lifespans or chemical composition dependency, such as heavy industry for materials and infrastructure, heavy transportation, petrochemicals, synthetics, and fertilizers.

Underinvestment in E&P and Its Consequences

Available, dependable and affordable fuels are hard to cancel. For example, the transition away from coal started about a hundred years ago. Its relative weight in the global primary energy matrix has dropped to about half since then but, as population has grown by four times and energy demand by a factor of almost ten, today we consume about five times more coal than in 1925. Similarly, hydrocarbons might reduce their proportional weight in the future global matrix but should nevertheless continue to supply stable or even growing absolute volume rates.

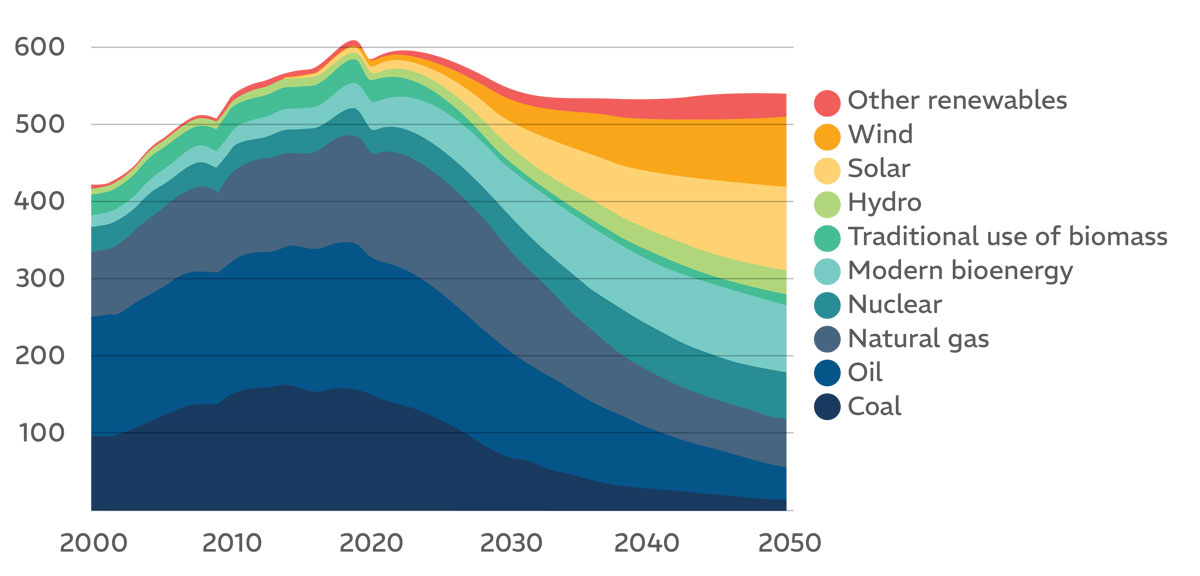

Some people seem to believe that if we just stop drilling for oil and gas — Presto!: renewable energy will magically fill the gap. But we should keep in mind that even the International Energy Agency’s most aspirational net zero CO2 emissions by 2050 scenario (figure 3) requires a continued supply of hydrocarbons beyond 2050. It is also obvious that this NZE’s scenario shows an energy demand peak in 2019 that did not materialize, nor seems likely to reach in the future. We also have a demand problem, not just a supply problem.

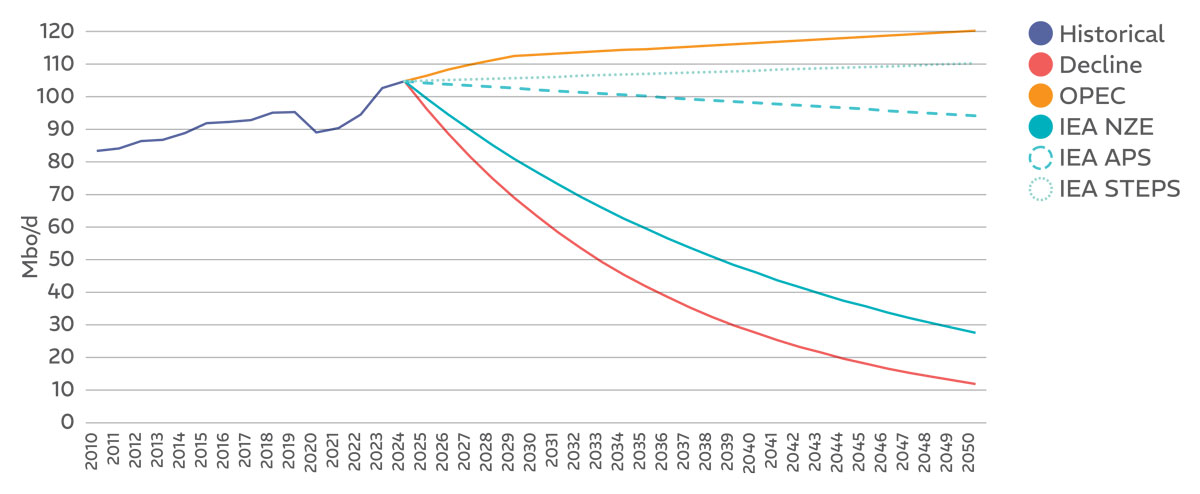

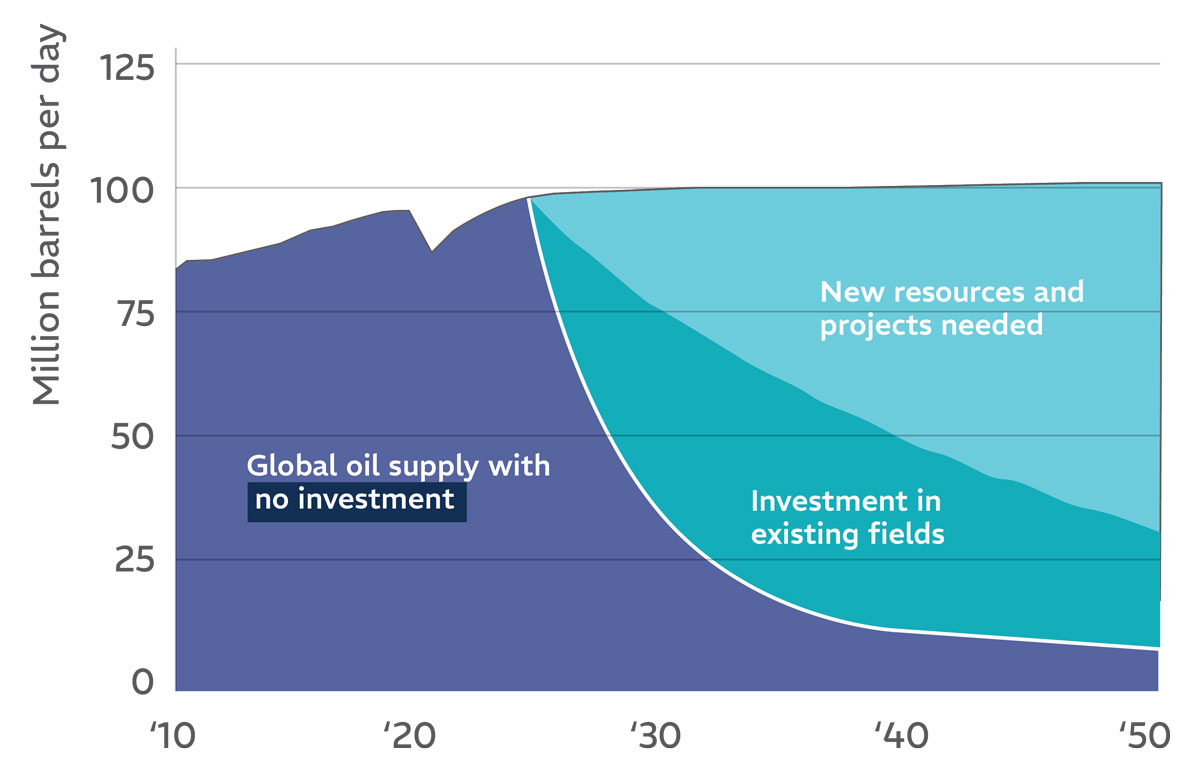

But as can be seen in figure 4, even if we magically stopped investing in drilling this instant, we would not adequately supply oil even for IEA’s NZE aspirational goal, not to mention the more realistic scenarios, such as Announced Pledges Scenario of government commitments and the Stated Policies Scenario. Our hydrocarbon output declines naturally and rapidly (we assumed 8-percent exponential from a 6-10-percent range, for illustrative purposes), so an energy security crisis and related price spikes would occur almost immediately.

Even departing from this extreme, if we plotted the crude production forecast for continuing investing in already existing producing fields only (no more exploration or even greenfield development, as per figure 5), it would track the NZE scenario, which is extremely unlikely to happen. If we develop the recently discovered resources but stop further exploring, the result would not be much better and should not reach STEPS or even APS either.

So, not exploring enough for new hydrocarbons will affect energy security, paradoxically revive coal, perpetuate the burning of biomass and quite likely lead to increases in the prices of energy products – a key component of general price inflation. This would generate economic hardship for the most vulnerable populations, economic distortions in energy-importing countries and fiscal losses for the producing countries.

Systems as complex as the ones involving energy, socioeconomic development and climate do not respond well to reductionist solutions, such as cancelling or choking our industry. In fact, due to the “law of unforeseen consequences,” these usually generate costly externalities or even worse. Such well-intentioned yet simplistic approaches have been imposed on our sector, while others have been self-inflicted.

Externally Imposed Restrictions

In 2020 the UN launched the “Race to Zero” campaign to rally leadership from various sectors to keep global warming not reaching 1.5-degrees Celsius, as called for in the 2015 Paris Agreement on the path to NZE by 2050. One of its reductionist mandates was to restrict the development, financing and facilitation of new fossil fuel assets.

A consequential and also reductionist initiative by multilateral and global commercial banks was to choke our industry from capital with the hope of in this way spurring the growth of renewables. In 2021 enthusiastic financial institutions launched the Glasgow Financial Alliance for Net Zero and committed to aligning their credit and investments with the NZE by 2050 objectives.

The UN’s hard approach (do not finance hydrocarbons, period, even for natural gas) generated concerns in global banks. A few major banks rebelled and began to abandon the Glasgow Alliance. The UN then published revised guidelines in 2022, withdrawing the requirements for banks to show a specific timeline and dropping the NZE by 2050 target, strictly speaking. The rigorous demand for banks to deny financing new hydrocarbon projects turned into a gentler requirement to gradually reduce their support to them. They had to backtrack.

Another reductionist “solution” by certain governments has been to deny new exploration licenses and/or to increase government take, thus either excluding our hydrocarbon industry from growth opportunities, or reducing its profitability to diminish its competitiveness vis-à-vis renewable energies. These short-sighted measures end up affecting such countries’ energy security, the cost of energy for their citizens, their fiscal accounts and paradoxically, their ability to leverage renewable energies with an uninterruptible basis.

Self-Inflicted Wounds

Large European international oil companies had vowed to aggressively evolve into clean energy companies to the detriment of their hydrocarbon portfolios (harvest what they had but end exploration and greenfield development). Some of them have had to backtrack under shareholder pressure because their returns shrunk.

We must acknowledge that it is not easy to transition from selling molecules to selling electrons. Different industries offer different idiosyncratic returns. Extracting global commodities with volatile prices and inherent exploration, exploitation and geopolitical risks yields commensurate margins. In contrast, generating electrons is less risky, but offers lower margins from domestic regulated prices. The required evolution in our legacy shareholder mindset requires acceptance of this new hybrid business model.

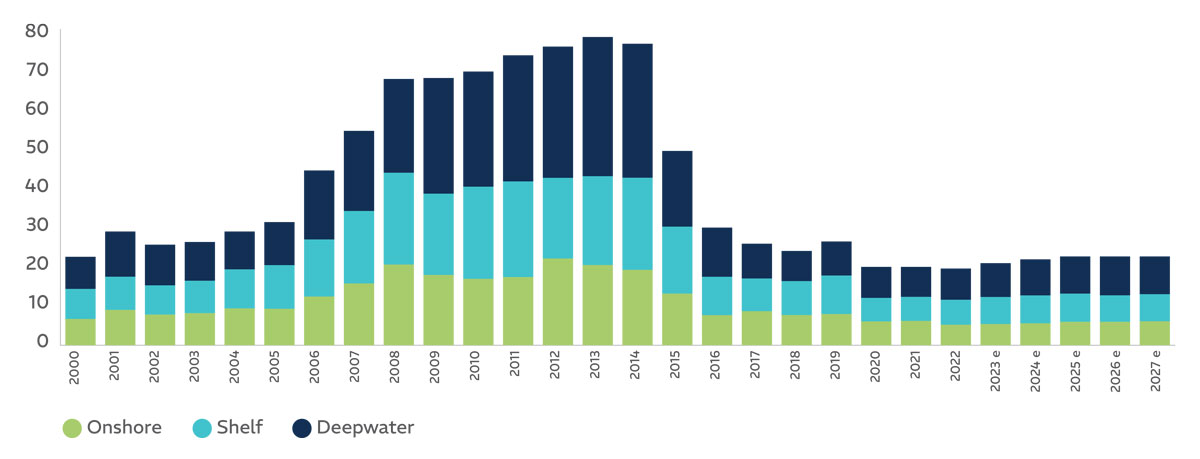

But besides, listed hydrocarbon companies are currently spending as much on dividends and share buybacks as in organic capital expense. Global exploration capital expense, for example, has dramatically dropped by 74 percent since their 2013 peak (figure 6). Not being able to replace their proven reserves organically, larger companies often tend to resort to inorganic growth via asset acquisitions and corporate mergers. That is just producing assets changing hands, not created. At this dismal exploration pace, it is not clear if we should worry first about peak demand or peak supply.

The Role of Governments in Attracting Capital

Developing countries cannot afford massive investments or hand out generous tax credits to private investors. They also cannot count on developed countries assisting them with capital for their energy transitions while assuring their energy security. From 2009 to 2015, developed countries had been pledging US$100 billion annually by 2020-2025 to help developing countries in their energy transitions. This pledge was broken, so today they promise $300 billion annually, which is still not even close to what global climate goals require.

Countries thus cannot rely on perennially-promised and trickle-delivered assistance. So, they must attract massive volumes of foreign direct investment, not only for renewable energies but also for exploration, development and production of hydrocarbons, of metal and critical minerals for expanded electrification, and to adapt/build the related infrastructures. But FDI is highly itinerant and finicky, and energy producing and developing countries must compete for less of it available.

Unless the perception of prospectivity is astonishing, hydrocarbon and energy investments of any kind usually have the same requirements: a favorable present conjuncture (government attitude, contractual and fiscal terms and resulting “take”) and, because of exposure due to considerable lead times to first revenue and to payout, the expectation of a long-term healthy investment climate (contractual stability, unencumbered capital flows, fiscal predictability and institutional quality). In brief, investments prefer legislative, fiscal, regulatory and judicial ecosystems that are solid, aligned, efficient, transparent and stable.

For example, it was hard for traditional international exploration to compete with the U.S. shale boom in the past decade. Several U.S.-based companies that had ventured internationally redirected their focus to the Eagle Ford, Bakken, Marcellus and Permian basins. These plays also attracted foreign companies, because they were prospective, quickly responsive and sat in the best hydrocarbon investment ecosystem on the planet. There is a reason behind the United States’ four-million-well history and why it is currently utilizing more than 60 percent of the global drilling rig fleet.

To enable similar virtuous systems, developing countries need to craft clear energy policies of state (not just of the incumbent government), reached by multiparty consensus, thus immune to ideological swings and electoral cycles. They often need better coordination within governments to streamline their environmental licensing and permitting processes for all forms of energy and for mining. Moreover, they need better cooperation among neighboring governments, beyond any ideological differences or old historical scars, seeking rational market and infrastructure integration and compatibility, and exploiting synergies between the competencies, inputs and energy sources that each can bring to the table.

National Oil Companies are Critical Participants

National oil companies hold almost 60 percent of global oil and gas proven reserves – more than two thirds in the case of Latin America and the Caribbean. According to Rystad Energy, half of all global production growth between 2025 and 2030 will come from NOCs, lifting their market production share above 50 percent. These companies and their resources sit in the developing world.

They must often attract partners and capital. Those institutions still under close government control should exercise more governance and financial autonomy to stay competitive and make nimble decisions under the current uncertainties. Ideally, not unlike the policies of state already mentioned, they should also be insusceptible from electoral/ideological cycles.

Latin America and the Caribbean Have Much to Offer

Our region’s astoundingly prolific Atlantic margin is open to private investment and shows superior above-ground competitiveness. Whilst LAC contributes only 10 percent of oil and 5 percent of natural gas to global output, according to S&P Global it has yielded 38 percent of all hydrocarbon resources discovered worldwide since 2020, 32 percent just among Brazil, Guyana and Suriname.

It also holds about 500 trillion cubic feet of gas resources in Argentina’s Vaca Muerta shale and offshore along the Colombia to Brazil margin. These resources should foster further integration, reduce emissions in the cleanest regional primary energy matrix and can generate exportable gas surpluses that may help reduce the incidence of coal in other longitudes.

In summary, hydrocarbons will continue to provide the bedrock of energy security for the conceivable future. We should not ask ourselves if we should stop exploring and developing, but if we are doing enough of it. Reestablishing appropriate exploration investment levels in our sector requires dismantling barriers, both external and internal. LAC governments should attract the necessary capital by offering sound investment ecosystems. Their NOCs have a crucial role to play in growing hydrocarbon production and should have more freedom in setting and pursuing their growth goals.