Growing demand for natural gas has reshaped the energy landscape in the United States in a big way.

Case in point: the mega-merger between independents Devon Energy and Coterra Energy announced in February, creating a gas-production behemoth.

Meanwhile, companies are positioning themselves to take advantage of projected higher U.S. natural gas prices and a strong demand outlook, especially on the Gulf Coast. Several recent deals have involved Haynesville shale gas assets.

“The big stories in natural gas right now are the phenomenal growth in LNG export capacity, aiding the push toward gas becoming more of an international resource, and the second one is increased domestic usage driven by data center load growth,” said Andrew Dittmar, principal analyst for Enverus Intelligence Research.

“In the longer-term outlook, it’s put the commodity in a stronger position than it has been in in years,” he noted. The U.S. Energy Information Administration released its first projections for 2027 in January. The EIA forecast a slightly lower average Henry Hub natural gas spot price this year, climbing sharply to $4.59 per million Btu next year. It projected U.S. LNG exports to rise from 15 billion cubic feet per day last year to 18.1 Bcf/d in 2027.

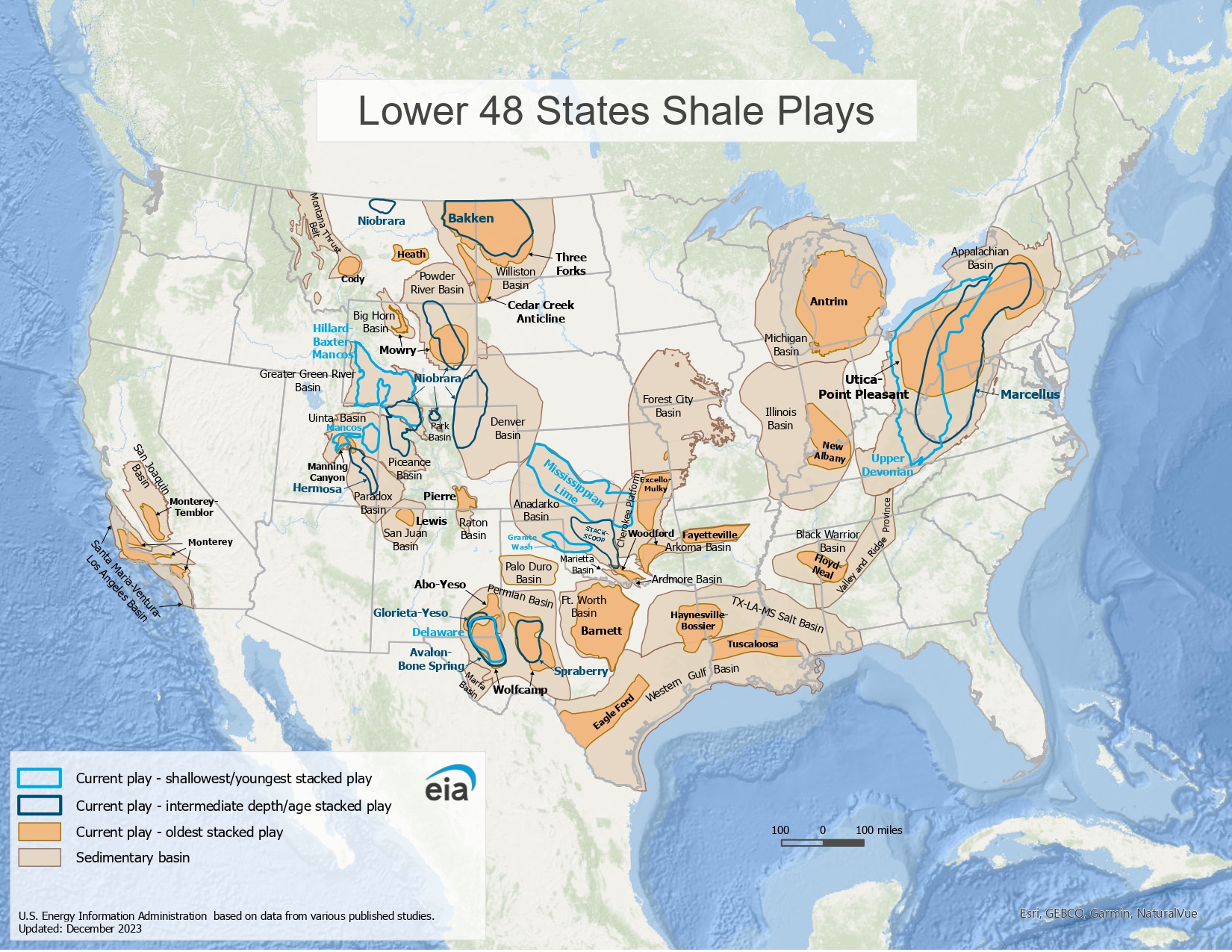

A New Shale Giant

Devon Energy reported its merger with Coterra will create one of the world’s leading shale producers. On a pro forma basis, combined third-quarter 2025 production would exceed 1.6 million barrels of oil equivalent per day, including 4.3 Bcf/d of gas and more than 550,000 barrels of oil per day.

The deal includes nearly 750,000 net acres in the core of the Delaware Basin shale play, Devon noted. Based on its stock closing price, it put the combined enterprise value of the merged companies at approximately $58 billion.

“The deal propels Devon from the third largest to top producer in the prolific Delaware Basin based on gross operated volumes, and positions it as a top three overall Permian producer on a gross operated basis with more than 1 (million barrels of oil equivalent per day),” Dittmar wrote in an analysis for EIR.

“The Delaware Basin, and particularly the northern portion located in New Mexico, holds some of the best quality rock in North America,” he added.

In announcing the deal, Devon reported it had identified $1 billion in annual pre- tax synergies. Analysts speculated the combined company also might divest some properties and production, possibly from its Marcellus shale play holdings.

“Overall, Devon will have operations across six major plays (after the merger) including a new position in the Marcellus. No divestment target was given as part of the deal, but the combined company could capitalize on a robust market for asset sales to trim its portfolio,” Dittmar wrote.

He noted the Marcellus play “contributes about 42 percent of Coterra’s total net production or 2 (billion cubic feet of gas equivalent per day)”.

The merger “was really focused on the Delaware Basin, with the secondary part being the Anadarko (Basin). It remains to be seen what they do with the Marcellus,” he said.

Other Major Mergers

Consolidation of Permian Basin shale assets has been going on for several years through a series of large mergers and property acquisitions. Now activity has picked up in several other U.S. basins as companies strengthen their gas production positions.

“The most notable example of that is the influx of mostly Japanese buyers who want exposure to U.S. gas supply,” Dittmar said.

U.S. shale gas producing properties, especially those near Gulf Coast LNG facilities, are attractive as a hedge against rising natural gas prices for Japanese energy companies that contract to buy and distribute natural gas and LNG supply.

In January, Mitsubishi Corp. announced it had agreed to acquire all equity interests in Aethon III LLC, Aethon United LP and related entities for about $5.2 billion plus more than $2.3 billion in assumed debt. The deal is expected to close by the end of June, pending regulatory approvals.

“Aethon’s shale gas assets are primarily located in the Haynesville Shale formation, spanning Texas and Louisiana, and currently produce approximately 2.1 Bcf/d of natural gas (equivalent to about 15 million tons per year of LNG),” Mitsubishi reported.

In a recent research note, energy information and analysis firm Wood Mackenzie observed “the Haynesville shale in Louisiana and eastern Texas is particularly attractive because it is close to many of the LNG export facilities of the Gulf Coast.

“Wood Mackenzie estimates that once the Mitsubishi/Aethon deal closes, Japanese companies will control about a third of the production in that formation,” it noted.

JERA Co., Japan’s largest power generation company, reported in October last year it would pay $1.5 billion to acquire all of Williams Upstream and GEP Haynesville II LLC holdings in the Haynesville shale’s South Mansfield gas asset.

Conducted through the company’s JERA Americas subsidiary, the deal involved production of more than 500 million cubic feet/day and includes a future investment plan to increase total production to 1 Bcf/d.

“The Haynesville Acquisition builds on JERA’s substantial and growing presence in the United States, including its recent announcement of the largest offtake of U.S. LNG from a single buyer – 5.5 million tonnes (metric tons) per year for 20 years – and the Blue Point low-carbon ammonia development project. JERA also owns, in whole or in part, 10 power generation assets across the country,” the company reported.

A year ago, TG Natural Resources acquired a 70-percent interest in the East Texas gas assets of Chevron USA for $525 million, with $75 million paid in cash and $450 million as a capital carry to fund Haynesville development. TG Natural is indirectly owned by Tokyo Gas, Japan’s largest natural gas utility.

In late 2023, TG Natural announced it was acquiring Rockcliff Energy II LLC, a portfolio company of Quantum Energy Partners, for $2.7 billion. Rockcliff was focused on developing the Haynesville shale in East Texas with more than 1.3 Bcf/d of gross operated gas production.

“It’s really remarkable how much of the Haynesville has transferred from domestic producers to these international groups, about 4 billion cubic feet a day of gross operated production,” Dittmar said.

Consolidation’s Next Chapter

After a series of substantial transactions, future merger and acquisition activity in the Permian Basin might be slowing down, although it’s undoubtably not over.

“Permian gas has continued to grow even in a low oil price environment,” Dittmar noted.

“The Permian is really consolidated now, with a tremendous amount of M&A attention focused on the Delaware and Midland basins in recent years,” he said.

There’s a similar situation in the Haynesville play, where companies have been positioning themselves in the natural gas market through numerous acquisitions and divestments in recent years. Attention has started shifting more to other gas production areas like the Anadarko Basin that also can feed Gulf Coast gas demand.

“The Haynesville is really almost off the table now in terms of new acquisition opportunities,” Dittmar observed.

“Natural gas has played a big part in revitalizing Anadarko M&A. I think there’s more coming up in the Anadarko this year – Ovintiv is planning on selling assets,” he said.

Last year, Ovintiv Inc. announced plans to divest around $2.5 billion in Anadarko Basin assets to pay down debt, starting in the first quarter of 2026.

“We’ve seen an uptick in development activity in the San Juan Basin, spearheaded by LOGOS Energy,” Dittmar said.

Development activity also has increased in the Utica Basin shale, where EOG Resources acquired premier acreage positions from Encino Acquisition Partners for $5.6 billion in 2025.

And the Appalachian Basin has become an emerging hub for data-center buildout near existing natural gas production.

“The more interesting story for Appalachia is bringing the demand to the gas, instead of the gas to the demand,” Dittmar said.

Looking ahead, energy companies are confident in growth for U.S. LNG exports, and they’re keeping a close eye on AI-related data center plans.

“I think we have to be a little more cautious on (predicting) gas burn for data centers versus LNG demand,” Dittmar said.