In 2023, America took over the title from Australia as the world’s No. 1 liquefied natural gas exporter. Gas superpower Qatar is a close third. America has been increasing its lead ever since. With strong government support from the Trump administration, among other factors, America is positioned to enhance that lead substantially in coming years. International companies – both developers and importers of LNG – are trying to be part of the expansion.

LNG’s Growing Demand

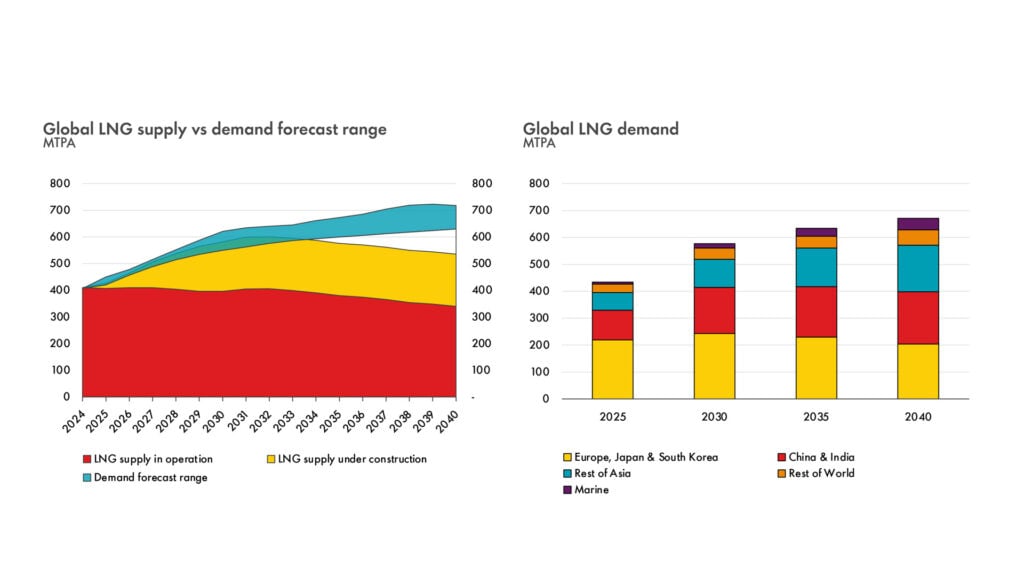

According to Shell’s “LNG Outlook 2025,” global LNG trade reached a new record of 407 million tonnes in 2024. Global LNG demand is on pace to increase around 3 percent annually to reach between 620 – 710 million tonnes by 2040.

The traditional major demand centers of Japan, South Korea and Europe will continue to import around 200 million tonnes in the coming two decades, peaking at 2030 at 220 million tonnes per year.

In the meantime, China and India are the new Japan and South Korea, growing their LNG demand significantly. By 2035, the world’s two most populous countries will import around 200 million tonnes of LNG. The other Asian countries will make up for the bulk of additional growth, from 60 million tonnes per annum in 2025 to 170 MTPA in 2040.

More than 50 countries have become LNG importers from the days when Japan and South Korea were by far the two biggest LNG importers. With the Russian invasion of Ukraine and Europe trying to become independent of Russia pipeline gas, Europe’s demand for America LNG is also growing fast.

In many parts of the world, gas is replacing coal for power generation. Gas is also expanding to power marine transportation.

The Growing LNG Supply

According to the Institute for Energy Economics and Financial Analysis, the world will add on average 42 MTPA LNG supply capacity per year between 2025 and 2028. More than 70 percent of the growth will come from the United States and Qatar.

The United States now has an LNG capacity of 94 MTPA. Final investment decisions have been taken for 80 MTPA projects that are under construction and due to come on stream before 2028. Projects with a combined capacity of 60 MTPA have received U.S. government approval and await final investment decision. By the mid-2030s, total U.S. LNG export capacity could grow to around 250 MTPA, or more than one third of the global LNG demand at that time.

Qatar’s North Field has more than 1,000 trillion cubic feet of gas resources and the world’s most price competitive LNG supply. The country is increasing its capacity from 77 MTPA now to 140 MTPA by 2030 with participation of leading LNG producers Shell, ExxonMobil, TotalEnergies and ConocoPhillips to assist with technology, and Chinese and Japanese companies to provide market support.

Australia, on the other hand, is projected to lose its LNG export leadership position due to three reasons: its feed gas is more expensive than either Qatar or the United States, its growing domestic gas demand, and Australia has stricter environmental regulations for lower carbon emissions. Operation issues, such as higher down time for some Australia LNG projects, have also contributed to a negative perspective.

Russia certainly has the gas resource base to become a major LNG exporter, but its political challenge is unlikely to disappear as international investors will hesitate to invest in major Russian LNG projects any time soon.

Canada has become the world’s latest LNG exporter after Shell brought LNG Canada to operation in the second quarter of 2025. Canada LNG can reach Asian markets from the Pacific coast without going through the Panama Canal, saving significant shipping time and cost. Canada LNG has a strong potential to grow. However, since the feed-gas needs to be supplied from inland basins via long-distance pipeline, Canadian projects have some ways to go to become more cost competitive as a major LNG supplier.

Traditional LNG exporters Algeria, Indonesia, Malaysia and Egypt are gradually losing their importance. From now until 2040, LNG export capacity from these countries will decrease from 50 to 5 MTPA, unless there are major new discoveries or developments.

US LNG Industry Enjoys Strong Government Support

The U.S. LNG industry is perhaps that industrial sector that has enjoyed the strongest government support since President Trump returned to the White House.

One day after Trump’s inauguration, the Department of Energy issued a statement to reverse Biden’s LNG permitting pause. Government support ranges from accelerated approvals for LNG export permits to non-Free Trade Agreement countries, to less restrictive environmental scrutiny, to increased incentives for foreign countries and companies to buy more U.S. energy products, especially LNG, and increased investments in U.S. energy projects.

For example, under the trade deal reached with Trump administration, the European Union will purchase $750 billion by 2028 in U.S. energy (including LNG, oil and nuclear technology) and make $600 billion new investments in the United States. The new agreement would require a significantly higher level of EU imports of American energy products. In 2024, total EU energy import from the United States amounts to less than $80 billion – or less than half of the annual average required between 2025 and 2028.

For the trade deals with Japan and South Korea, these two Asian countries are committed to invest $550 billion and $350 billion in the United States, some of which will be likely in energy projects, such as LNG. South Korea also committed to purchase $100 billion energy products from the United States.

The trade negotiations between the United States and China are still ongoing. It is expected that China will commit to substantially increase imports of U.S. energy products, especially LNG. That will be required to reduce the trade imbalance between the world’s two largest economies. Political tensions between the United States and China, however, are expected to create some reluctance by Chinese companies to invest in U.S. energy projects.

US LNG Supply is Going Fast

Cheniere Energy is by far the biggest American LNG exporter with 53 MTPA export capacity in commercial operation. It is deploying a brown-field expansion strategy, planning to increase its capacity to 75 MTPA by 2030 from its two sites Sabine Pass and Corpus Christi in Texas. Cheniere has an ambition to become a 100-MTPA supplier in the future.

Venture Global LNG is becoming the second largest LNG exporter with 36 MTPA export capacity now its two projects, Calcasieu Pass and Plaquemines, are moving into commercial operations. Venture Global recent arbitration win against Shell is giving it a new momentum.

San Diego-based Sempra has 28 MTPA either in commercial operation or being constructed. It has another 13.5 MTPA of Phase 2 in Port Author and is positioned to rival Cheniere and Venture Global LNG.

Another emerging pure play LNG producer Next Decade is still without actual production, though it is trying to complete three trains in Rio Grande LNG with 15 MTPA capacity. Next Decade says that it will start delivering LNG by 2027.

LNG heavyweights Qatar Energy and partner ExxonMobil had to manage the challenge of the Golden Pass LNG when the lead contractor Zachry declared bankruptcy. ExxonMobil said that the partnership now expects first LNG production later in 2025. It is interesting to note that Qatar’s original plan was to partner ExxonMobil to import Qatar LNG to the U.S. market.

Another international LNG leader, Woodside has taken over a Louisiana LNG project after acquiring LNG developer Tellurian in 2024. Woodside could double its LNG capacity to 33 MTPA in Louisiana LNG if it can take final investment decision for Phase 2, as the company is currently in the first phase of construction of three trains with 16.6 MTPA capacity.

The world has a history of struggling to balance the supply and demand of LNG. Elevated LNG prices will suppress demand, which will in turn lead to less investment in supply and market tightness.

This market volatility will continue, however, the overall strong LNG growth is inevitable.