While many are working to forecast when the price of oil might reach $80 a barrel again, renowned international strategist and geopolitical analyst Peter Zeihan predicts in stunning detail the rising and declining energy plays of 2025 and the countries that will ultimately triumph as the world’s leading producers.

Zeihan, the author of “The Accidental Superpower: The Next Generation of American Preeminence and the Coming Global Disorder,” was the keynote speaker at a November 2015 conference celebrating the 25th anniversary of Energistics, a nonprofit organization that manages the development and adoption of industry data management standards.

As if he were playing the games of chess and Risk simultaneously, Zeihan wove together factors of global recessions, changing demographics, civil unrests and the dance of supply and demand to support his theories on future energy power plays.

And, his predictions are so thoroughly supported with data and rich with geopolitical intrigue, Zeihan himself resembles a cross between a James Bond villain and an analyst for some military think tank (but much less menacingly, of course).

And Along Came Shale

Not only has shale oil turned the energy world upside down, Zeihan believes it is quickly paving the way for the United States to become energy independent by 2017.

Ever-evolving technologies, such as 4-D seismic, are eliminating the 20/80 rule – the idea that 20 percent of frac stages generate 80 percent of petroleum from shale fields.

“You know exactly where to go (in a formation). There is no guessing. This has dropped the use of inputs – whether that’s skilled labor, sand, or water or chemicals – by two-thirds,” Zeihan said. “Cross that over with new drilling techniques that are now becoming industry standard … and the results are mind blowing.”

Five years ago, wells went down a mile and extended laterally by 600 feet. Two years later, they reached out a mile. “That’s a ten time increase in drilling capacity per pad,” he said. “Then they started combining surface infrastructure, and you have upwards of 20 straws going into the ground in the same place. Your surface costs have now dropped about three-quarters.”

Zeihan predicted that one straw attached to 20 or 30 miles of lateral pipe will be industry standard by the end of 2016.

“Think of what that does to input costs,” he said. “We are not in an energy production recession in the United States. We are in an energy input recession. That’s very different.”

Zeihan believes the break-even costs in the shale patch soon will be at $35, perhaps even $30, a barrel.

“That will make shale cost-competitive with every oil production zone in the world outside of the Persian Gulf,” he said. “Imagine what’s going to happen when re-frac’ing becomes industry standard.”

Era of Decline

Consumption of energy has dropped in the United States, beginning with the 2008 recession and oil prices reaching $80 a barrel, prompting many to buy hybrid automobiles – ultimately cutting American demand by 2 percent, Zeihan said. Combine those factors with the fact that Baby Boomers, the largest generation ever seen in the United States, are beginning to retire and drive less, and demand is undoubtedly decreasing.

“The United States is looking at at least 15 – probably closer to 25 – years of secular demand decline even with oil prices at $40 a barrel,” he noted.

Furthermore, with the advent of shale energy, the United States is now importing oil from six locations instead of 30.

“We are seeing the end of the American import story,” Zeihan said, explaining that net imports to North America are less than 3 million barrels per day and will continue to decline as advanced hydraulic fracturing technology becomes the norm.

In Europe, demand is declining as well – mostly because of its financial crisis, Zeihan said. “The Europeans were looking at secular demand decline even before you consider the recession that they’ve pretty much been in for the last seven years,” he said. “That means less inflows of energy.”

“Throw in the Russians and they are starting to dominate the oil matrix of Western Europe, and the only place you can go (to sell oil) is Asia. So the Asian premium … instead of being $3 to $8 a barrel, it’s like 50 cents to maybe $1.50. Not nearly as exciting,” Zeihan said.

Add to that the reality that the United States is becoming less interested in the wider world and no longer needs to provide naval security for global maritime free trade, as was established in the Bretton Woods system of monetary management in 1944. The United States’ motivation for sustaining that system was to buy alliances with other countries for economics and security, and to ultimately win the Cold War, Zeihan said.

“Only 7 percent of our GDP came from exports last year, and half of that was from NAFTA (North American Free Trade Agreement),” Zeihan said. “So we’ve got a global system that the Americans designed to fight a war that ended 25 years ago. This is the culmination of the Americans stepping back from the global system a little bit every year for the last 25. And very soon the plug will be pulled.”

The Domino Effect

Having set the global stage of today, Zeihan began to predict the consequences of the United States’ shale boom and simultaneous disinterest in the wider world:

With Asia being the primary market for oil, the Asian premium is inverting at a time when there is overproduction.

“A system this lopsided cannot possibly last,” he said.

Secular demand is changing, but more importantly, secular supply is too. A crack in the Middle East, a crack in the Russian system and a crack in East Asia – all of which are leading toward sharp supply declines in the world’s major basins and an inability to get what’s left of that supply to East Asia – and the following breakdowns begin to take place:

The Canadians, who have supplied oil to the American Midwest, are trying to negotiate a series of pipelines to the American Gulf of Mexico refineries so its heavy sour crude can be mixed with the United States’ light, sweet oil from shale for a medium blend, which existing refineries can process without being retooled. If these pipelines – “the Keystone being the loudest one” – cannot be negotiated, Canada’s Athabasca Region will likely shut down, Zeihan surmised.

Looking at Russia, Zeihan pointed out that the country is becoming imperialistic to secure its borders, knowing its army is dwindling on account of a low birth rate since the end of the Cold War.

“The entire western periphery of Russia stands out from the rest of the geography, from the rest of the world, because the highest physical barrier between the Russian populations and everybody else is about the same elevation as an interstate on-ramp in Kansas,” Zeihan quipped. “There’s nothing there that stops people from marching in.”

Zeihan believes Russia’s goal is to expand to include the Caucasus, the Carpathians, the Polish Gap and the Baltic Sea countries to shrink its western periphery from 3,000 miles to roughly 600.

“Militarily, it’s not a challenge. The countries around Russia are weaker than Russia is. The only question is timing,” Zeihan said. “If you move forward three or four years when it has really sunk into the Americans that they can go on their own and be alright, then we enter a world where we look to the French to convince the Germans to invade Poland to fight off the Russians, which if you follow your history is not a preposterous concept.”

In this conflict, it is not out of bounds for Russia to cut oil and natural gas supplies to other countries as a political tool prior to an invasion, Zeihan said. Or, its targets might cut the supply chain to give the Russians pause. “Either way you are looking at 6 million barrels of crude per day and 150 billion cubic meters of natural gas facing some degree of threat,” Zeihan said.

Strategy

Here is how Zeihan foresees the conflict erupting: Once the Russians invade the Baltic countries, Sweden will lead an alliance to join in. When the Russians invade Poland, the Germans will feel no choice but to jump in. Zeihan said Russia believes it can handle the Swedes and the Germans, yet it will not be able to do that in the midst of a third conflict with Turkey.

Therefore, Russia must launch a distraction strategy to bring the Turks out of the coalition – “which brings us to Syria,” Zeihan said. The Fertile Crescent area of Syria contains 60 percent of the population and 95 percent of the food production. While ISIS does not inhabit that area, it could.

“Do you ever associate ISIS rulership with state agricultural output?” Zeihan asked. “Russia’s plan is simple. Remove the barriers in play so that ISIS can get to the Syrian heartland, and if you have a three-way war between the rebels, the government and ISIS, you generate a famine and 15 million refugees. All of them have to go to Turkey.”

Zeihan added more color to his analysis: “Regardless of whether or not Turkey just shoots everyone at the border, invades in order to impose stability on Syria, tries to process them, or tries to pass them through to the Europeans – no matter what choice Turkey makes, strategically, it is occupied for at least half a decade, which means the Turks don’t have a free hand to intervene in the Ukraine or the Caucasus. Russia has removed Turkey from play. It’s a brilliant move. Morally, horrific. But strategically brilliant.”

Conflict in the Persian Gulf

On another front, as the Americans slowly pull out of the Persian Gulf, potential for conflict will heat up, Zeihan predicted, with the Saudis and Iranians opposed politically, economically and strategically.

“Because of shale they are now exporting the same product along the same routes going to the same countries. But really, think of this as the Texas A&M and UT rivalry, just with more guns,” he said. “And like all great rivalries, eventually fans end up on the wrong side of the border in the wrong bar.”

Speaking of Iran and Saudi Arabia alone, 11 million barrels per day of crude production could be at stake. “That assumes nobody gets caught in the crossfire,” Zeihan said. “That assumes that the war, the conflict, doesn’t spread anywhere else. And it will.”

He reminded that there are eight major conflicts currently taking place in the Middle East, and the Saudis and the Iranians are opposed in all eight of them.

“The Saudis are using their checkbook diplomacy to fund, arm and create groups as they need, and the Saudis are winning in six of those eight conflicts. Syria is an example of a conflict where the Saudis are winning. ISIS gets funding from Saudi Arabia,” Zeihan said.

“What will be really fun is when the day comes for artillery to be exchanged and the Iranians will fall back on the strategy they’ve had the last four years: Try to close the Gulf, which will convince everybody in the global system to put pressure on the United States to end this, to prevent a global energy recession,” Zeihan said.

At that point, however, the United States will likely have lost interest, he continued. “In fact, I expect the Saudis to help. Because to fight the Iranians, the Saudis have a bypass pipeline. They can get 5 million barrels of crude out.”

Therefore, Iran loses all export capacity for a period of time, and things begin to look bleak for Iraq, Kuwait and Qatar as well, Zeihan said. “You’re looking at potentially 20 to 25 million barrels of crude that just can’t get out,” he said.

On Asia’s Shoulders

Moving eastward, Zeihan pointed out a third global conflict that could arise in Northeast Asia. “If we get into a position where we have an absolute shortage of crude, remember why the Asian premium has existed since the Nixon administration. It’s a long sail – no suppliers – all the way to Northeast Asia,” he said.

“If there is a reduction in output anywhere, the entirety of the impact is felt in Northeast Asia. Northeast Asian countries – all of them – are navally capable. And if the U.S. isn’t providing the security, they will have no choice but to deploy their own navies to the Persian Gulf, pick sides in the Middle East and … then escort crude back home to their home countries,” Zeihan said.

Speaking tongue-in-cheek, he added, “As we all know, the Chinese, the Japanese, the Koreans and the Taiwanese have a long – centuries long – history of cooperation and brotherly appreciation. There’s no chance whatsoever that anything could go wrong in any of that.”

Escaping Energy Disruptions

While Zeihan predicted that energy disruptions are essentially guaranteed in Russia-Europe, Saudi Arabia-Iran, and Northeast Asia, countries and regions that will likely escape the turmoil include: the United States, Mexico, Central America, Australia/New Zealand, Indonesia, Malaysia, Myanmar, Philippines, Vietnam, France, United Kingdom, Denmark, Netherlands, Sweden, Switzerland, India, Argentina and Turkey.

“These are locations that are geographically secure, physically secure in the future and have neutral-to-strong and grown demographies,” Zeihan said.

A big piece of his reasoning – at least for the United States – is California, which is now the nation’s largest oil importer. Fast-forward two years and it may be the only one, Zeihan said.

“That’s fantastic … because you have access to American levels of security and protection, but a near bottomless local import market,” he said.

Currently, California imports roughly 800,000 barrels per day. It sources more than half from the Persian Gulf. Although Kern County, Calif., has not yet been able to get into shale because of the cost, it likely will have a breakthrough soon, Zeihan said.

“Here you have a system where you can produce crude locally or in Alaska,” Zeihan said. “Alaska, by a quirk of American law, is exempt from the export ban. So $50 crude for the long haul is really depressing … but if you can sell it for $150 in California, well hot damn. If you can produce in Alaska, which actually has a regulatory environment that you guys enjoy, and then sell that abroad, hot damn.”

“So it’s not the wider world but this – in terms of security and risk/reward – this looks brilliant,” he said, adding that the United States, Mexico and Central America will have “rock bottom” energy prices because of shale.

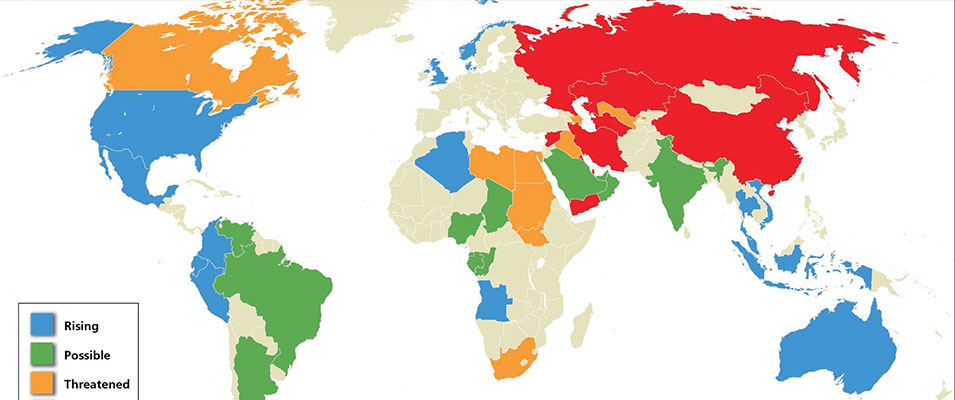

Rising Plays of 2025

Combining countries’ physical security, demographics and energy producing potential, Zeihan presented a predictive map of energy plays in 2025 that ranked countries from to “rising” to “declining.”

Rising countries include: the United States, Mexico, Colombia, Ecuador, Peru, Australia, Indonesia, Vietnam, Thailand, Angola, Algeria, United Kingdom, Norway and Denmark.

“These are places where investment is good and security is good. The production horizons vary country by country, but you should see a pretty strong expansion,” Zeihan said.

Countries that may encounter obstacles include Saudi Arabia, Argentina, India, Nigeria, Brazil and Venezuela.

In “declining” countries such as Russia, Kazakhstan, China, Yemen and Iran, Zeihan said, “I can’t see a scenario where we will be seeing more crude or better operating conditions in these countries.”

Zeihan ended his vision for the future of energy where he began – with shale. “Canada, Mexico, the United States, Argentina and Australia – that’s it for shale in the appreciable volumes. For everyone else, it’s whether they can sustain a relationship with an outside power,” he said.

The United States, the “accidental superpower,” comes out on top. “There’s nothing in the broader external system,” Zeihan said, “that could really threaten the United States in a systematic way.”